Kymriah is a transformative autologous cell therapy drug from Novartis Pharmaceuticals, approved by FDA this month aimed at treating refractory ALL in pediatric and young adults. Studies have shown up to 83% remission and this being first-in-class, with relatively small addressable population (estimated to be ~600 patients per annum), it is widely believed that a $475,000 price tag is reasonable. Adding to woes of patient access, Novartis and States Centers for Medicare and Medicaid Services (CMS) have agreed upon a first of its kind outcome-based pricing model, where the payment is made only after a month’s time if the performance of the drugis visible. This path breaking approval sets precedence in multiple areas, first of which being FDA’s readiness to approve complex cell therapy drugs. This also comes at the backdrop of a recent major event involving acquisition of Kite Pharma by Gilead for its CAR-T therapy against B-cell lymphoma and Kite’s first MAA in EMA for this drug. With an exciting future for cell therapy, there are already efforts underway to solve some of the major short comings of the first generation cell therapies. These include reducing the number of production days and reducing drug complexity by using mass produced allogenic stem cells which do not require multiple hospitalizations. Such a promising therapy from a leading big pharma gives reason to expect a number of new innovations in the theme of “drugs by the bed” (bedside modification and infusion) and non-personalized, yet effective allogenic therapies.

Kymriah is a transformative autologous cell therapy drug from Novartis Pharmaceuticals, approved by FDA this month aimed at treating refractory ALL in pediatric and young adults. Studies have shown up to 83% remission and this being first-in-class, with relatively small addressable population (estimated to be ~600 patients per annum), it is widely believed that a $475,000 price tag is reasonable. Adding to woes of patient access, Novartis and States Centers for Medicare and Medicaid Services (CMS) have agreed upon a first of its kind outcome-based pricing model, where the payment is made only after a month’s time if the performance of the drugis visible. This path breaking approval sets precedence in multiple areas, first of which being FDA’s readiness to approve complex cell therapy drugs. This also comes at the backdrop of a recent major event involving acquisition of Kite Pharma by Gilead for its CAR-T therapy against B-cell lymphoma and Kite’s first MAA in EMA for this drug. With an exciting future for cell therapy, there are already efforts underway to solve some of the major short comings of the first generation cell therapies. These include reducing the number of production days and reducing drug complexity by using mass produced allogenic stem cells which do not require multiple hospitalizations. Such a promising therapy from a leading big pharma gives reason to expect a number of new innovations in the theme of “drugs by the bed” (bedside modification and infusion) and non-personalized, yet effective allogenic therapies.  USFDA’s approval of Mvasi (bevacizumab) by Amgen and Allergan, marks the beginning of the era of approval of biosimilars with oncological indications. The drug, though not interchangeable with the original product, has been approved for all the indications of the original product including colorectal cancer, lung, glioblastoma, kidney and ovarian cancers.

USFDA’s approval of Mvasi (bevacizumab) by Amgen and Allergan, marks the beginning of the era of approval of biosimilars with oncological indications. The drug, though not interchangeable with the original product, has been approved for all the indications of the original product including colorectal cancer, lung, glioblastoma, kidney and ovarian cancers.

While this signifies continuing regulatory openness for biosimilars, the WHO‘s pilot program for prequalification of biosimilars comes as an added boost to the biosimilars industry. Created to provide greater access for essential drugs and API qualified by standard procedures to low and middle income countries (LMIC), WHO PQ program has established success in accelerating approval timelines, enhancing regulatory capacity and more importantly improving health outcomes and up-take of low cost generics in LMIC. In the pilot, WHO has proposed two pathways, one for biosimilars approved by stringent regulatory authorities (FDA, PMDA etc.) and the other pathway for drugs approved by other national regulatory authorities. This project will begin in October 2017, when WHO will publish it first expression of interest covering rituximab and trastuzumab. While the RoW markets have the highest need for biosimilars to expand healthcare access, we had highlighted in our White Paper that, level of penetration of biosimilars in RoW markets is very disappointing so far and RoI is elusive. The WHO PQ program is very promising as it holds the potential to expand markets in LMIC by introducing clinical confidence in product quality and use as a lower cost substitute to otherwise unaffordable biologics. After EMA and USFDA flagging in their approvals, WHO stepping in could imply that Era 3.0 for biosimilars is finally here.

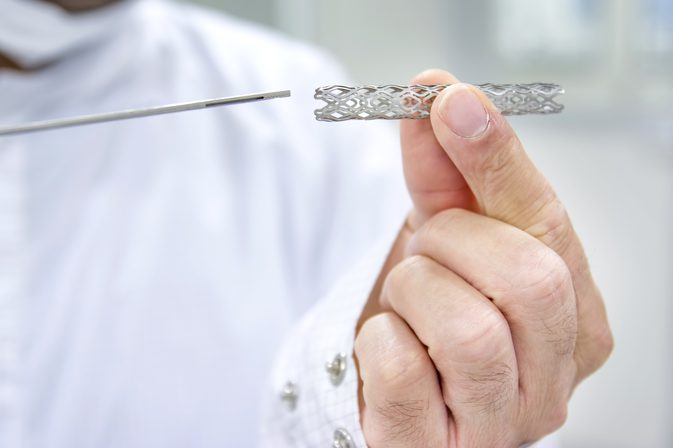

Abbott has globally halted sales of its2 bio absorbable stents, Absorb and Absorb Gt1 this month, citing low commercial sales. Global sales has been discontinued from 100 countries including India, effective from the 14thof September. Earlier heralded as the next generation of cardiac stents, the product was available in Indian and European market since 2012 and was cleared by USFDA in July 2016. However, it has come into close regulatory scanner with red flags in the post monitoring data. Boston Scientific has also planned to cease its BVC development after Abbott’s decision and Indian player Meril’s product is currently under regulatory review. The withdrawal points to criticality of post monitoring data for product validation as well as for inducing clinical confidence in novel technologies. This comes at a pertinent time when several countries across the world (including India) begin to emphasize Phase IV studies and roll out more robust requirements. While this development sends the latest technology wave in interventional cardiology to the trenches, it also threatens to slow down device innovation due to concerns around potentially higher investments for future product development, if larger clinical studies with longer follow-up periods are required.

Abbott has globally halted sales of its2 bio absorbable stents, Absorb and Absorb Gt1 this month, citing low commercial sales. Global sales has been discontinued from 100 countries including India, effective from the 14thof September. Earlier heralded as the next generation of cardiac stents, the product was available in Indian and European market since 2012 and was cleared by USFDA in July 2016. However, it has come into close regulatory scanner with red flags in the post monitoring data. Boston Scientific has also planned to cease its BVC development after Abbott’s decision and Indian player Meril’s product is currently under regulatory review. The withdrawal points to criticality of post monitoring data for product validation as well as for inducing clinical confidence in novel technologies. This comes at a pertinent time when several countries across the world (including India) begin to emphasize Phase IV studies and roll out more robust requirements. While this development sends the latest technology wave in interventional cardiology to the trenches, it also threatens to slow down device innovation due to concerns around potentially higher investments for future product development, if larger clinical studies with longer follow-up periods are required.

It is also interesting to note that while Absorb had lukewarm sales in Europe and most global markets, it was popular in India and had a relatively larger share of the market. As a largely out-of-pocket market with limited participation of qualified payors in determining pricing, top quartile of patients of the otherwise price sensitive market have been easier and less discerning payors for expensive new medical technologies.

FDA 483s and manufacturing issues have been one of the primary reasons for recent value erosion in many generic pharma companies. The threatnow appears to have seeped into the biologics world as well. Case in point is FDA rendering South Korean biopharma giant, Celltrion, on back foot, issuing a form 483 with 12 observations for their biosimilar facility in Incheon, South Korea. While most critical observations were around issues with vial stoppers, others issues were observed in relation to occurrence of foreign matter in the drug substance as well as drug product. FDA has also pointed out aseptic conditions as a common reason backing several observations. While Celltrion continues to express confidence about quality of its export batches, this development is likely to impact sales of Inflectra, the biosimilar version of J&J’s Remicade developed by Celltrion with partner Pfizer, which was green signaled by FDA last April. While the industry continues to grapple with the burgeoning regulatory scrutiny in small molecule pharma, this new trend is unsettling, calling imminent attention of the industry to raise the bar in manufacturing quality. In the biosimilars arena where the quantum of investment is several fold higher and RoI is yet to be realized, product recalls and facility shutdowns could be detrimental and potentially even threaten survival. Unflinching attention to quality is quintessential.

FDA 483s and manufacturing issues have been one of the primary reasons for recent value erosion in many generic pharma companies. The threatnow appears to have seeped into the biologics world as well. Case in point is FDA rendering South Korean biopharma giant, Celltrion, on back foot, issuing a form 483 with 12 observations for their biosimilar facility in Incheon, South Korea. While most critical observations were around issues with vial stoppers, others issues were observed in relation to occurrence of foreign matter in the drug substance as well as drug product. FDA has also pointed out aseptic conditions as a common reason backing several observations. While Celltrion continues to express confidence about quality of its export batches, this development is likely to impact sales of Inflectra, the biosimilar version of J&J’s Remicade developed by Celltrion with partner Pfizer, which was green signaled by FDA last April. While the industry continues to grapple with the burgeoning regulatory scrutiny in small molecule pharma, this new trend is unsettling, calling imminent attention of the industry to raise the bar in manufacturing quality. In the biosimilars arena where the quantum of investment is several fold higher and RoI is yet to be realized, product recalls and facility shutdowns could be detrimental and potentially even threaten survival. Unflinching attention to quality is quintessential.  Geographic growth, diversification and reorganization have all driven the M&A landscape across the healthcare continuum this month. Adding momentum to the trend of emerging market companies investing in North America and Europe, Chinese biotechnology firm 3SBio and its private equity partner CITICPE have acquired the Canada based contract development and manufacturing (CDMO) business of Therapure for USD 290 Million. Additionally, 3SBio has also secured rights to Therapure’s plasma products and technology for the Chinese market and agreed to further invest C$ 20-25 million in construction of new commercial facility. In the medical devices world,niche neonatal device company Natus Medical Corporation has diversified into the neurosurgical market with $47.5 million deal to acquire from Integra Lifesciences,the Camino’ ICP monitoring product linealong with a manufacturing plant, U.S. rights to fixed pressure shunts,DURAFORM® dural graft implant, standard EVD catheters and CSF collection systems.

Geographic growth, diversification and reorganization have all driven the M&A landscape across the healthcare continuum this month. Adding momentum to the trend of emerging market companies investing in North America and Europe, Chinese biotechnology firm 3SBio and its private equity partner CITICPE have acquired the Canada based contract development and manufacturing (CDMO) business of Therapure for USD 290 Million. Additionally, 3SBio has also secured rights to Therapure’s plasma products and technology for the Chinese market and agreed to further invest C$ 20-25 million in construction of new commercial facility. In the medical devices world,niche neonatal device company Natus Medical Corporation has diversified into the neurosurgical market with $47.5 million deal to acquire from Integra Lifesciences,the Camino’ ICP monitoring product linealong with a manufacturing plant, U.S. rights to fixed pressure shunts,DURAFORM® dural graft implant, standard EVD catheters and CSF collection systems.As Teva seeks to revitalize its operations under renewed leadership and divest its Women’s Health, Oncology and Pain management businesses, it has exited its intrauterine copper contraceptive product PARAGARD® to CooperSurgical for USD 1.1 billion. The company has decided to strengthen its strategic focus on its core business areas of CNS and respiratory, and is envisioning to use the proceedings to invest in a strong pipeline within these segments. Roche has become the second big pharma this month to streamline business focus, with their divesture of manufacturing facility to Swedish firm Recipharm AB. This deal comes as part of Roche’s restructuring strategy for its small molecule manufacturing in order to reinforce its newer generation therapeutics and more specialized manufacturing.

We have previously highlighted the popularity of co-marketing agreements in improving market entry and access, especially in India. Recent events in the pharmaceutical industry has further reinforced this trend in India and other Asian markets such as Korea. Building on a slew of market partnerships across insulin, DPP4 inhibitors and vaccines, Lupin has announced the intent to extend the model to a GLP-1 agonist to bridge the gap in its diabetes portfolio. A very similar deal has been signed in South Korea, where CKD pharma has signed a joint-marketing agreement with Amgen for Prolia (Denosumab). This is also the first deal between a big pharma and Korean firm for a biologic drug. This agreement entails CKD marketing the drug in small and medium hospitals and neighborhood clinics while Amgen retains the rights to market the drug in big hospitals. This is a classic example that demonstrates the merit in utilizing established local assets in difficult to penetrate market segment sand expanding markets in a synergistic manner. Going forward, we anticipate this trend to continue and sale force strength of the potential local pharma partners will become a key deciding factor while innovative product company make such choices. This increased willingness to partner is also reflective of the infection point in the pharmaceutical industry as a whole, where revenues are under pressure, global markets matter more than ever and there is greater inclination to pursue innovative partnership, marketing and pricing models.

We have previously highlighted the popularity of co-marketing agreements in improving market entry and access, especially in India. Recent events in the pharmaceutical industry has further reinforced this trend in India and other Asian markets such as Korea. Building on a slew of market partnerships across insulin, DPP4 inhibitors and vaccines, Lupin has announced the intent to extend the model to a GLP-1 agonist to bridge the gap in its diabetes portfolio. A very similar deal has been signed in South Korea, where CKD pharma has signed a joint-marketing agreement with Amgen for Prolia (Denosumab). This is also the first deal between a big pharma and Korean firm for a biologic drug. This agreement entails CKD marketing the drug in small and medium hospitals and neighborhood clinics while Amgen retains the rights to market the drug in big hospitals. This is a classic example that demonstrates the merit in utilizing established local assets in difficult to penetrate market segment sand expanding markets in a synergistic manner. Going forward, we anticipate this trend to continue and sale force strength of the potential local pharma partners will become a key deciding factor while innovative product company make such choices. This increased willingness to partner is also reflective of the infection point in the pharmaceutical industry as a whole, where revenues are under pressure, global markets matter more than ever and there is greater inclination to pursue innovative partnership, marketing and pricing models.